Do you ever have the nagging feeling that you should hold some gold “just in case.” You might already hold some. Perhaps gold is a major component of your portfolio. But does it belong in your portfolio? What is gold’s investment value?

Here are the three reasons people might want to add gold to their portfolios.

- In some future crisis, gold might become money.

- Gold is often said to be a good inflation hedge.

- Gold is an interesting speculative investment – its price has risen a lot recently.

I discussed gold as currency and as a hedge against inflation in two previous articles. What about gold as an investment?

Gold as an investment

Belief 3: Gold will go up in value just as it has in the past. Like stocks and bonds, it should be part of my investment portfolio.

Gold is not a productive investment asset. It does not pay interest like a bond. It does not pay dividends like a stock. Gold’s only potential source of return is an increase in its price.

There is no reason to anticipate gold’s price to increase. As a commodity, its value depends on its uses and the costs of alternatives in those uses. For example, gold is popular as jewelry. If it becomes more popular as jewelry, its price would tend to rise. But popularity is a matter of taste. The evolution of tastes is unpredictable.

When we considered gold as an inflation hedge, we saw that it has gained value (about 116%) in purchasing power terms since January 1979.

To be sure, there have been times when gold appreciated much more dramatically. From March 2001 to August 2011, gold’s real price rose a whopping 447%. From May of 2019 to December 2020, the price increase was 43%.

However, there have been large losses as well. For example, from January 1980 to June of 1982, gold lost 61% of its purchasing power. That’s bigger than the Great Financial Crisis stock market decline. The earlier chart showing gold’s price over time in 1979 dollars illustrates the rather dramatic recent history of its price gains and losses.

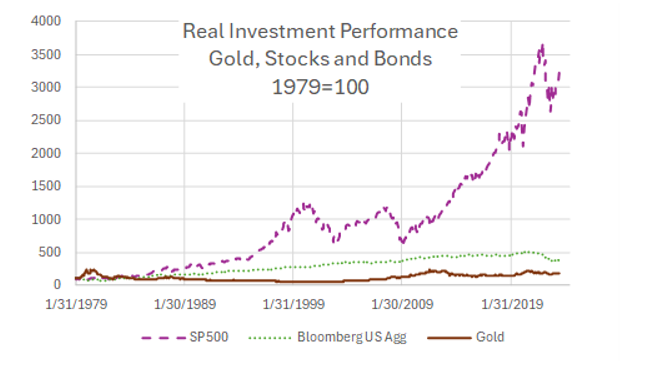

Now I’m going to compare gold to US stocks and US bonds from an historical investment perspective. I’ll use the S&P 500 index for stocks, and the Bloomberg US Aggregate Bond index for bonds. I’ll adjust all of them for inflation. The chart below illustrates that both stocks and bonds have dramatically outperformed gold since 1979. I’ve adjusted each asset to 100 in January 1979 to make it easy to compare returns visually.

The table below compares average investment returns and risk (measured by standard deviation) for the three assets. Gold has average annual returns equal to bonds (both 3.4%), and risk greater than stocks (21% and 15.9%). Low return and high risk is not an attractive combination. In general, expected return should be higher for riskier assets to encourage investors to hold them. [Note: the total return for gold is about half that of bonds over this period: gold ends up at about 217 vs bonds at 379 using 1979 as 100 as the graph illustrates. Even though average annual returns are equal, gold’s much greater risk reduces the long-term realized total return relative to bonds.]

1979-2023

Summing up

We’ve considered three possible reasons investors might want to hold gold:

- As a possible future currency or money

- As an inflation hedge

- As an investment

In the case of currency, commodity currencies like gold and silver were once dominant, but in the last 100 years or so, fiat currencies have largely swept the field.

Gold’s price movements appear to be independent of inflation, making it a poor inflation hedge at best. TIPS, especially short-term TIPS mutual funds, are almost certainly a better choice.

Finally, gold’s price is very volatile in the short term, and there are times when it increases sharply, but overall it hasn’t performed well as an investment since 1979 (when our data begin).

I wouldn’t claim that the evidence proves that investors shouldn’t hold gold. I think we can say that the case for gold is weak.

This article appeared originally in Forbes.com.

The foregoing content reflects Rick Miller’s opinions and is subject to change at any time without notice. Content provided herein is for informational purposes only and should not be used or construed as investment advice or a recommendation regarding the purchase or sale of any security. There is no guarantee that the statements, opinions, or forecasts provided herein will prove to be correct.

Past performance may not be indicative of future results. Indices are not available for direct investment. Any investor who attempts to mimic the performance of an index would incur fees and expenses which would reduce returns.

Securities investing involves risk, including the potential for loss of principal. There is no assurance that any investment plan or strategy will be successful.

Photo by Jingming Pan on Unsplash