You may not think about it much, but retirement accounts don’t have to be “set and forget”. Sure, you can move assets within retirement accounts into different funds and change your contribution amount, but you can also change the types of accounts you hold. Even after you’ve started a retirement account, either with an employer or independently, you can still make big changes. For example, you can convert a standard IRA (Individual Retirement Account) or 401(k) into a Roth IRA.

Why would you want to convert a traditional IRA or 401(k) to a Roth IRA?

The simple answer is to pay less tax in retirement. There is, however, a more detailed answer which requires an explanation. First, it’s important to establish what types of retirement accounts exist and what similarities and differences there are among them.

For the purposes of this article, we categorize retirement accounts as simply Roth IRAs or traditional IRAs. You can also convert to Roth accounts from many employer retirement accounts.

What is a traditional IRA?

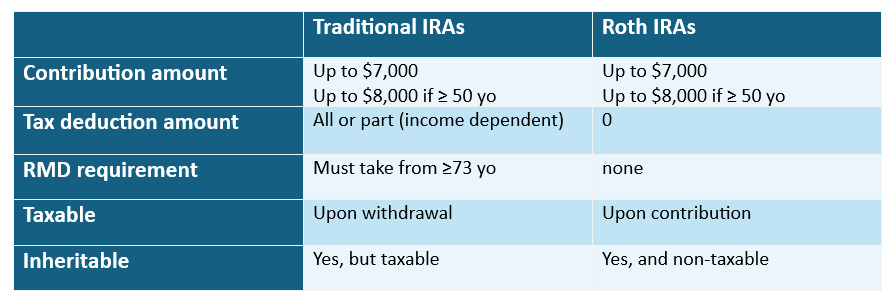

A traditional IRA is an account into which you deposit funds directly that you can draw from when you retire. You may also have an employer account such as a 401(k) or 403(b) which holds pre-tax retirement funds that you could roll into your IRA. Part or all the money you contribute to your IRA is tax deductible in the year you contribute, and taxable in the year you withdraw it.

In a traditional IRA, you can:

- Contribute up to $7,000 per year to an IRA (Individual Retirement Account), $8,000 if you are over 50.

- Deduct all or part of the contribution amount from your taxes depending on the your income.

And you must:

- Pay penalties for withdrawing funds before turning 59 ½ years old.

- Take RMDs (required minimum distributions) from age 73 onward.

- Pay tax on those RMDs.

Keep in mind that if you bequeath your traditional IRA accounts to your loved ones, they must pay the income taxes on those assets.

What is a Roth IRA?

A Roth IRA is a different type of retirement account. Like a traditional IRA, there is a limit to the amount you can contribute in a given year, and there are penalties for withdrawing funds before you turn 59½. Unlike a traditional IRA, you pay taxes on the income you contribute, but not when you withdraw.

With a Roth IRA, you can:

- Contribute up to $7,000 per year to an IRA (Individual Retirement Account), $8,000 if you are over 50 (but there is no income tax deduction).

- Withdraw your contributions tax-free at any time.

And you must:

- Pay taxes and a 10% penalty for withdrawing earnings before you turn 59 ½ (you also owe tax and penalty if you withdraw earnings before a five-year holding period after 59½.

Why would you want to convert a traditional IRA or 401(k) to a Roth IRA?

As I mentioned earlier, converting from traditional to Roth means you will pay less income tax in retirement. However, you will pay more tax before you retire. This trade is worth it if the total tax and IRMAA (income-related monthly adjustment amount for Medicare) you pay with the conversion is less than the total tax and IRMAA you’d pay if you didn’t convert.

What are the advantages of converting to a Roth account?

- You can withdraw from your Roth accounts without adding to your taxable income.

- You do not have to take RMDs, so you can choose how much and when you withdraw from your Roth accounts, giving you more control.

- You can bequeath Roth accounts to your heirs who will not pay income taxes on withdrawing from them.

- You may also avoid or reduce an IRMAA surcharge for Medicare.

What are the disadvantages in converting to a Roth account?

- You will have a larger than usual tax bill during the conversion year.

- You will gain a net advantage only as you live into retirement. If you live a shorter life, you may not see the payoff.

If you decide to convert some of your traditional IRA to your Roth IRA, it’s wise to consider your taxes for the year you make the conversion. Since you will pay taxes on the conversion amount, it makes sense to choose the optimal time to pay higher than usual taxes. Ideally, you’d pick a year in which your income is smaller than usual to allow you to pay a lower tax rate. That may be easier if your income fluctuates. If your income is steady, choose a year with more deductions, which may put you in a lower tax bracket.

Here’s the thing. To get the best result, compare your total lifetime income taxes and IRMAA payments with the conversion(s) to lifetime taxes and IRMAA with no conversions.

If there is an advantage, there will also be an ideal conversion pattern. This pattern is difficult to identify without a wizard or a complex algorithm. You must find the perfect balance of your income and tax rate for a given year, your age, your present or expected Social Security benefit amount, and the size of the conversion you want to make.

Since wizards are hard to find (when was the last time you saw a Gandalf look-alike wearing a conical hat and carrying a real magic wand?), many use software to determine the optimal year(s) for you to make Roth conversions.

What difference does it make when you convert?

If you pick the wrong year(s), you might end up paying more lifetime taxes and IRMAA with the conversion than without it.

Does how you pay the extra tax matter?

Yes, it does!

For example, if you convert $100,000 of your retirement fund to a Roth, you’ll pay approximately 25% tax or $25,000. You could pay it from the Roth account, which would pay the tax, but leave you with only $75,000 in the Roth. If, however, you pay the tax from a taxable savings account, you’ll be down the $25,000 in savings, but you’ll have $100,000 in your Roth, which is tax-free.

Converting to a Roth account has both advantages and disadvantages, and it’s not a one-size fits all proposition. Whether it’s the right decision for you depends on your income, age, the size of your retirement fund, risk tolerance, lifespan, and your plans. As with any financial plan, consult with your financial advisor before deciding.

Photo by Suzanne D. Williams on Unsplash